Retirement Income Strategy: Guardrails

May 3, 2023 • Written by Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Blog Home » Retirement Income » Retirement Income Strategy: Guardrails

Summary

- There are numerous variables involved in choosing an appropriate portfolio withdrawal strategy, most of which are unpredictable and outside of a retiree’s control (i.e. life duration(s), market volatility, inflation, unexpected expenses, etc.);

- Given the complexity and consequential nature of retirement income planning, it’s important to use a dynamic strategy (with explicit disciplined adjustments) throughout retirement in order to avoid (a) running out of money OR (b) unintentionally leaving behind a large legacy of money;

- We believe a risk-based Guardrails strategy is often the best approach for helping retirees navigate the complex financial landscape, achieving financial security, and providing a higher standard of living in retirement

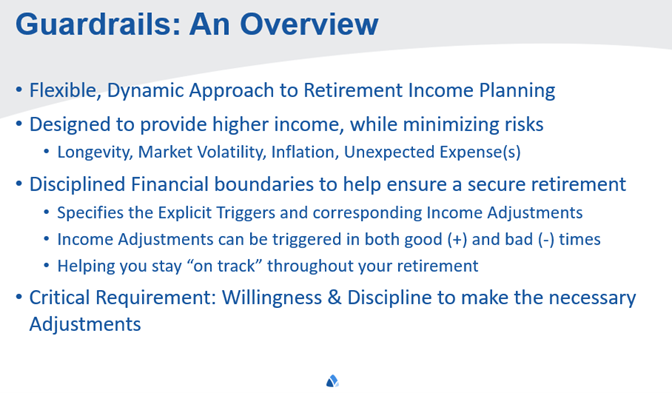

Guardrails Retirement Income Strategy: An Overview

Determining a retirement income withdrawal strategy is an important component in any retiree’s comprehensive retirement plan. Guardrails is a flexible, dynamic retirement income strategy that aims to adjust the amount of income withdrawn from retirement savings based on changes in financial market conditions, life events, and other factors that affect a retiree’s changing income needs over time. The basic idea behind this strategy is to adjust the retirement income distribution based on a set of predefined rules (or triggers) tailored to a retiree’s unique situation and preferences.

A guardrail retirement income strategy is designed to provide the highest possible retirement income, without jeopardizing your portfolio when (not if) the markets decline.

A guardrail dynamic retirement withdrawal strategy typically involves setting a base withdrawal amount from retirement savings (Four Factors Affecting Retirement Withdrawal Rates) and adjusting the amount (up or down) as necessary to reflect changes in the retiree’s investment portfolio value, inflation, and other factors that affect retirement income needs.

For example, if the market performs well and the value of retirement portfolio increases, the retiree may be able to increase their amount withdrawn. Conversely, if the value of retirement portfolio decreases to a predefined level, the withdrawal rate will need to be decreased to preserve savings and avoid the risk of running out of money in retirement. The pre-defined upper and lower boundaries serve as “guardrails”, ensuring the withdrawals don’t stray “off the road” (become too high or too low) based on changes to a retiree’s circumstances and market conditions.

When discussing guardrail “income adjustments” it’s important to understand that the income adjustments only pertain to income sourced from the portfolio; retirement income from other sources (i.e. Social Security, pension(s), annuities) would not be affected.

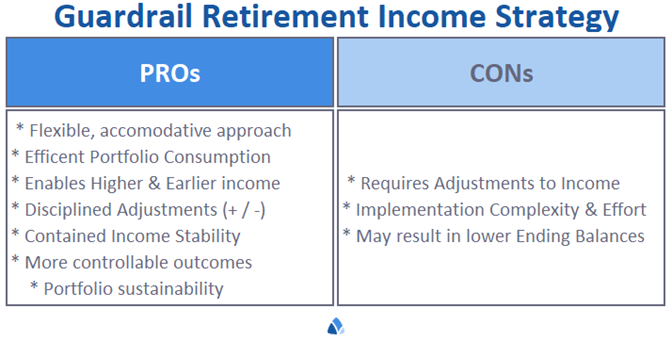

Using Guardrails: Pros and Cons

By incorporating disciplined income adjustments based on several factors (i.e. market conditions, retiree age, inflation, etc.) the guardrail dynamic withdrawal approach to retirement income planning allows for a higher level of retirement income, while minimizing risks of the unknown (longevity, market volatility, inflation, unexpected expense(s)). Retirees who can incorporate flexibility into their annual spending needs are able to set higher initial portfolio withdrawal rates. This can help better position a retiree to meet their near-term financial goals, especially to enable a more active lifestyle earlier in retirement. The disciplined, explicit triggers and corresponding income adjustments used in a guardrail strategy help ensure retirees stay on track throughout their retirement – keeping spending from drifting too high or too low in changing conditions. Additionally, the guardrail triggers and adjustments can be calibrated and tailored to meet a retiree’s personal goals and situation.

Retirees who can incorporate flexibility into their annual spending needs are able to set higher initial portfolio withdrawal rates.

Perhaps the biggest drawback of using a dynamic withdrawal strategy is that it’s relatively complex to monitor and implement year over year. Using a guardrail strategy requires determining an initial withdrawal rate, setting the explicit upper and lower guardrail triggers and the associated income adjustments, and managing and monitoring those over time. Due to the complexity and consequences of this, a retiree will likely need to engage a financial advisor specializing in retirement income planning, specifically with experience and expertise using guardrail withdrawal strategies. To use a dynamic withdrawal strategy, it’s also critical that a retiree have the willingness and discipline to make necessary adjustments (specifically, reductions) to their income as necessary.

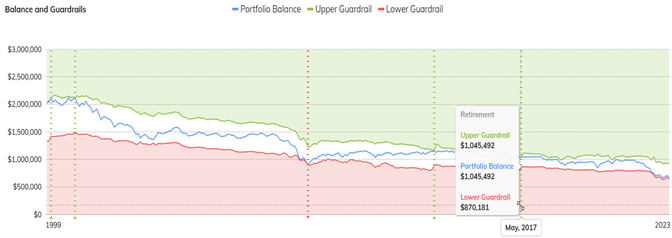

Guardrails: Conceptual

The diagram below is a hypothetical example using a guardrails retirement income strategy over a ~20-year period. As detailed in the diagram, the blue line represents the portfolio balance, with the green and red lines representing the upper and lower guardrails. The dashed vertical green and red lines indicate when a guardrail was triggered, and income was adjusted. Income was increased when the upper (green) guardrail was crossed, and conversely, income was decreased when the lower (red) guardrail was crossed.

While this is a hypothetical situation for illustrative purposes, the following items are reflective of outcomes retirees would commonly experience:

- In most years you remain within the Guardrails with no income adjustments required;

- Income Adjustments can be calibrated to be more aggressive, or conservative based on your personal goals and preferences (both in frequency of expected occurrences (triggers), and in magnitude of required income adjustments);

- Typically, there are more positive (income increases) than negative (income decreases) adjustments during retirement: in this ~20+ year example there were 4 increases and 1 decrease

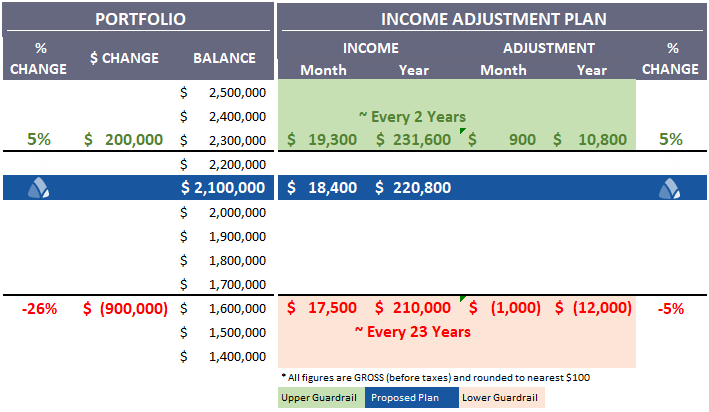

Guardrails In Action

The diagram above is one we at Staib Financial Planning use to manage and monitor our client’s retirement income plans. We (and our clients!) love it for its relative simplicity, and the breadth of information it provides. The items below summarize a few of the most important components:

- The upper guardrail is on the top in green and the lower guardrail is on the bottom in red. “You are here” is denoted by the blue horizontal bar. The leftmost 3 columns relate to the investment portfolio, with the rightmost columns relating to income.

- In this example, the client has a portfolio balance of ~$2.1 million, and a proposed annual gross income of $220,800 (~$18,400/mo).

- The upper guardrail would be triggered if the portfolio value increased by ~$200k (or ~5%) to ~$2.3 million. If this were to occur, the retiree’s income could be increased by ~$10,800/yr (~$900/mo) to ~$231,600.

- The lower guardrail would be triggered if the portfolio value decreased by ~$900k (or ~-26%) to ~$1.6 million. If this were to occur, the retiree’s income could be decreased by ~$12,000/yr (~$1,000/mo) to ~$210,000.

- The illustration also contains general expectations regarding the anticipated frequency with which the guardrails would be triggered. In this example, the upper guardrail would be triggered about every 2-3 years, while the lower guardrail would be triggered about every 23 years, or 1-2 times during a traditional 30 year retirement.

- Our retirement income guardrail illustration is also valuable in performing “what if” scenario assessments. For example, if this client was considering making a $100k RV purchase, we could quickly assess that this was feasible as the expenditure would result in the retiree remaining comfortably within the guardrails (~$2.1m portfolio is reduced to ~$2m; moving the retiree “one lane” closer to the lower guardrail, but still comfortably above it).

Guardrail Retiree: Ideal Profile

To use a dynamic withdrawal strategy, it’s critical that a retiree have both the willingness and discipline to make necessary adjustments (specifically reductions) to their income as necessary.

While there is no one-size-fits-all retirement income approach appropriate for all retiree’s, a guardrail strategy often checks several of the boxes for many retirees. Below is a listing of characteristics that would make it a strategy worth considering:

Pre-Requisite: Willingness & Discipline to make the necessary Income Adjustments!

- Desire Higher Income, Earlier in Retirement

- Knowledge and Understanding of Expenses:

- Relatively High Discretionary expenses (able to adjust)

- Relatively High Stable Income (social security, pension(s)…)

- Preference for higher Retirement Income than higher ending Legacy

- Willingness to have relatively higher equity allocation throughout retirement (~60%-80%)

- Desire income flexibility; have “ad hoc” spending plans

- Approach retirement planning as ongoing process (vs event)

- Willingness to engage professional expert(s)

Summary

Retirement income guardrails are a set of strategies or guidelines that can help retirees protect their retirement income by minimizing the risks of longevity, market volatility, inflation, and unexpected expenses. These guardrails are designed to help retirees stay “on track” throughout their retirement, adjusting income from the investment portfolio as conditions (i.e. age, investment portfolio balance, expenditures, etc.) change over time.

The guardrails are financial boundaries to help ensure a secure retirement. The guardrails can be triggered in both good times (ability to increase spending) and in bad times (need to reduce spending). A critical component of utilizing a guardrail approach to retirement is the willingness and discipline to make the necessary adjustments as conditions merit change, much as you likely have done throughout your life up to retirement (i.e. layoffs, salary freezes/increases, promotions/bonuses, etc.).

We believe the guardrail approach is the best approach for helping retirees navigate the complex financial landscape of retirement and achieve financial security. Contact us if you are interested in learning more how a guardrails strategy can improve your security, confidence and standard of living in retirement.

Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Paul Staib, Certified Financial Planner (CFP®), RICP®, is an independent Flat Fee-Only financial planner. Staib Financial Planning, LLC provides comprehensive financial planning, retirement planning, and investment management services to help clients in all financial situations achieve their personal financial goals. Staib Financial Planning, LLC serves clients as a fiduciary and never earns a commission of any kind. Our offices are located in the south Denver metro area, enabling us to conveniently serve clients in Highlands Ranch, Littleton, Lone Tree, Aurora, Parker, Denver Tech Center, Centennial, Castle Pines and surrounding communities. We also offer our services virtually.

Read Next

Panic and Greed: Ineffective Investment Strategies

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

If markets are good at one thing, it’s reminding investors that stock prices don’t simply go up, uninterrupted, forever. Markets…

Investment Strategy…using an Index Card

• Written By Paul Staib | Certified Financial Planner (CFP®), MBA, RICP®

Harold Pollack, a professor of public policy at the University of Chicago, generated a good deal of buzz a few…